The aircraft, engine and parts manufacturing industry is climbing due to rising fleet replacement and global air travel, which is driving demand for more commercial aircraft and associated parts.

Key Statistics Snapshot according to IBISWORLD:

Market Shares for key US players:

| The Boeing Comp | 33.9% |

| GE Aviation | 8.5% |

| Lockheed Martin Corporation | 7.7% |

| United Technologies Corporation | 6.7% |

Airlines around the world are seeking to upgrade their fleet to newer, more fuel-efficient models. In particular, economic growth in the U.S. and in emerging markets has increased global air travel traffic and enticed airlines to expand their fleets. Year-over-year passenger travel growth for the past five years has averaged 6.2 percent. Low air fares, higher living standards with a growing middle class in large emerging markets, and the growth of tourism and travel relative to total consumer spending in major economies are all driving strength in the demand for air travel.[1] As a result, Boeing and Airbus have surplus demand for aircraft, with combined backlog orders of over 9,000 commercial aircraft.

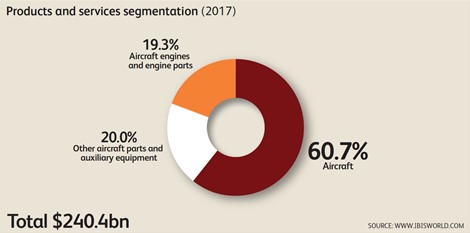

Breakdown of the total US revenue of $240 B

Key External Drivers:

- Demand from air transportation

- Federal funding for defense

- Non-Nato defense spending

- Trade-weighted index (The trade-weighted index (TWI) measures the value of the US dollar against the currencies of its largest trading partners. A decreasing TWI leads to lower export prices and higher import prices.

The United States is prepared to soak up this demand. The U.S. is the largest aircraft manufacturer in the world, and is home to the leading companies in the large commercial aircraft, combat aircraft, helicopters, unmanned aerial vehicles and engines segments. In the commercial aircraft segment, Boeing dominates, as it is the only U.S. manufacturer of medium to large size airliners. Since U.S. companies like Boeing hold such a strong market position, any increase in demand by international airlines for new aircraft typically leads to increased demand for U.S. planes.

In a 2015 PwC report, the U.S. was ranked as the top location for commercial aircraft manufacturing. Countries were ranked on several variables, including costs, industry size, and infrastructure/stability/talent. The U.S. ranked first out of 142 countries, despite only moderate grades in the cost and infrastructure/stability/talent categories, because it’s the largest in terms of industry size.

U.S. companies are seeing enormous opportunities to partner with foreign firms in hopes of gaining market shares in new regions. U.S. manufacturers across the supply chain – from makers of engines to electronics and communications systems to airframe parts – have already made quick strides to partner with emerging aviation manufacturers, but this looks to be simply the beginning of a much more globalized industry.

Expansion in global markets carries numerous risks, including but not limited to intellectual property protection, talent recruitment, training, and retention.

Finding a right partner for manufacturing in dollars might be a huge opportunity to drive your global business further.

COGNEGY has successfully worked with foreign companies in advanced industries who want to enter the U.S. marketplace. COGNEGY’s Atlanta, Washington, Philadelphia locations, staff of C-level executives and extensive experience provides foreign firms with a hands-on, trusted partner well versed in the local business climate to map out an partner search and acquisition or a customized plan for corporate growth.

Please contact COGNEGY with any questions you might have: e-mail phil.jafflin@cognegy.com or call +1 (404) 917-7100 extension 903

[1] Boeing Current Market Outlook, 2017-2036, page 7

[2] http://usblogs.pwc.com/industrialinsights/2014/01/20/globalization-pressures-lessons-from-the-us-aircraft-industry/